Bookmark this page - Add to your tool bar.

Welcome to my Interest Rate News page... please feel free to call me, Irene, or Denise with any questions you may have.

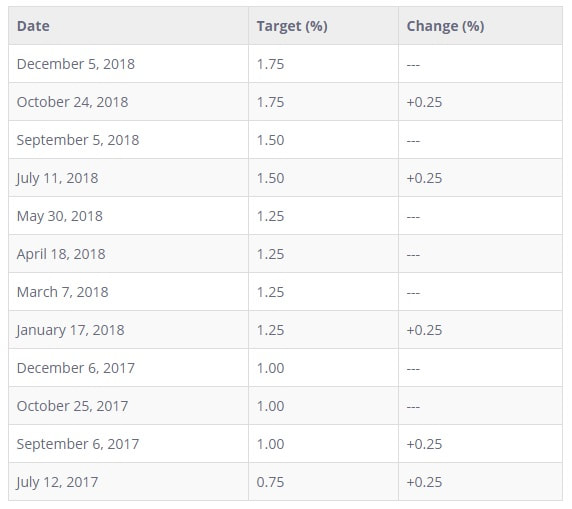

BANK OF CANADA HOLDS KEY INTEREST RATE AT 1.75%

NEWS RELEASE - FOR IMMEDIATE RELEASE

Media Relations 613-782-8782 Ottawa, Ontario December 5, 2018 The Bank of Canada today maintained its target for the overnight rate at 1 ¾ per cent. The Bank Rate is correspondingly 2 per cent and the deposit rate is 1 ½ per cent.The global economic expansion is moderating largely as expected, but signs are emerging that trade conflicts are weighing more heavily on global demand. Recent encouraging developments at the G20 meetings are a reminder that there are upside as well as downside risks around trade policy. Growth in major advanced economies has slowed, although activity in the United States remains above potential. Oil prices have fallen sharply since the October Monetary Policy Report (MPR), reflecting a combination of geopolitical developments, uncertainty about global growth prospects, and expansion of U.S. shale oil production. Benchmarks for western Canadian oil – both heavy and, more recently, light – have been pulled down even further by transportation constraints and a buildup of inventories. In light of these developments and associated cutbacks in production, activity in Canada’s energy sector will likely be materially weaker than expected. The Canadian economy as a whole grew in line with the Bank’s projection in the third quarter, although data suggest less momentum going into the fourth quarter. Business investment fell in the third quarter, in large part due to heightened trade uncertainty during the summer. Business investment outside the energy sector is expected to strengthen with the signing of the USMCA, new federal government tax measures, and ongoing capacity constraints. Along with strong foreign demand, this increase in productive capacity should support continued growth in exports. Household credit and regional housing markets appear to be stabilizing following a significant slowdown in recent quarters. The Bank continues to monitor the impact on both builders and buyers of tighter mortgage rules, regional housing policy changes, and higher interest rates. Inflation has been evolving as expected and the Bank’s core measures are all tracking 2 per cent, consistent with an economy that has been operating close to its capacity. CPI inflation, at 2.4 per cent in October, is just above target but is expected to ease in coming months by more than the Bank had previously forecast, due to lower gasoline prices. Downward historical revisions by Statistics Canada to GDP, together with recent macroeconomic developments, indicate there may be additional room for non-inflationary growth. The Bank will reassess all of these factors in its new projection for the January MPR. Weighing all of these developments, Governing Council continues to judge that the policy interest rate will need to rise into a neutral range to achieve the inflation target. The appropriate pace of rate increases will depend on a number of factors. These include the effect of higher interest rates on consumption and housing, and global trade policy developments. The persistence of the oil price shock, the evolution of business investment, and the Bank’s assessment of the economy’s capacity will also factor importantly into our decisions about the future stance of monetary policy. Information noteThe next scheduled date for announcing the overnight rate target is January 9, 2019. The next full update of the Bank’s outlook for the economy and inflation, including risks to the projection, will be published in the MPR at the same time. k here to edit.

Historic Rate changes

More self-employed hitting mortgage wall because of recent rule changes

For years, mortgage brokers self-employed clients could count on getting a mortgage on the strength of their credit score, and on their word that they were earning enough from their business to repay the loan. These days, because of rules brought in almost two years ago by the regulator of the country's chartered banks, borrowing money to buy a home has become harder for many of the country's 2.75 million self-employed workers – a group that, according to Statistics Canada, has a higher median net worth than paid employees. "We went through years and years when my clients who were self-employed could get a mortgage if their credit score was 680 or higher, with next to no documentation, "Today clients going in to their bank for mortgage refinancing and they're shocked because suddenly they're no longer approvable." In the summer of 2012, the Office of the Superintendent of Financial Institutions introduced Guideline B-20, which required federally regulated banks to tighten their processes for approving mortgages and home equity lines of credit. As part of B-20, banks must now look more closely at incomes before approving a mortgage application. This presents a problem for self-employed workers, who typically lower their taxable income by maximizing business expenses and personal deductions. Because of the discrepancy between what's on their tax return and how much money they actually earn, self-employed workers have typically obtained their mortgage through "stated income" applications, which required a signed income declaration and proof of self-employment such as a business registration number or articles of incorporation. Today, self-employed workers can still apply for a stated income mortgage at some banks, but under B-20 they can borrow only 65 per cent of the purchase value – 10 per cent less than what was allowed before B-20 – without requiring default insurance from Canada Mortgage Housing Corp., Genworth Canada or Canada Guaranty. "If you have less than 35-per-cent down payment, your mortgage now has to be insured, and insurers have specific guidelines that you need to meet," says Ms. Green. "For example, CMHC will allow a stated income application as long as you have been self-employed for less than three years. More than three years and you have to qualify according to your net taxable income." So what can self-employed workers do to improve their chances of qualifying for the mortgage they need, on terms that work for them? coming in with complete and current financial and tax documents is critical. Lenders usually ask for the latest notice of assessment from Canada Revenue Agency and financial statements from the past two years. "We may also ask to see bank statements to show regular income going into your bank account. Raza Hasan, senior vice-president for retail lending and wealth-management risk management at Canadian Imperial Bank of Commerce, says self-employed borrowers need to make sure they are up-to-date with income and sales tax returns, and that they don't owe taxes. They also need to be ready to explain their business. "It's very important that you be able to discuss the details of your business – your income, expenses, at what point in time you will break even, your business milestones," Mr. Hasan says. "Then we can look at that and find the right solution for you." The more information a bank has, the better it can help self-employed borrowers qualify for the mortgage they want, says Ms. Green, whose client base is made up largely of self-employed workers. "Certain lenders allow add backs of things like car expenses, capital cost allowance or housing expenses," Ms. Green says. "These add backs then enable the applicant to qualify for what they want to buy." Some lenders take a different approach to increase the mortgage eligibility of self-employed workers. Vancity Credit Union in Vancouver, for one, adds 15 per cent to reported income and will boost the percentage if the self-employed borrower provides financial statements showing deducted business expenses totalled more than 15 per cent. Ms. Green notes that credit unions are not affected by B-20 and many still extend a mortgage of up to 80 per cent of purchase value to stated-income applicants without the need for default insurance. For sole proprietors or owners of an unincorporated business, making the leap to incorporation could also help, says Jeff Hull, senior financial adviser at Manulife Securities Inc. "Most banks prefer salary, and if you have a corporation you can pay yourself a salary," he says. "That may make it easier for a self-employed individual to qualify for a mortgage." Incorporating could also reduce tax rates and allow the business owner to collect a higher salary or dividend payout, Mr. Hull adds. Courtesy of The Globe & Mail MARJO JOHNE SPECIAL TO THE GLOBE AND MAIL PUBLISHED MARCH 24, 2014 UPDATED MARCH 25, 2017 |

Mortgage Rates

Dec 5, 2018 - this weeks rates 5 year closed term HR 3.49% (quick close, by Jan 31st) 5 year closed variable HR 3.00% 5 year closed LR 3.69% (80% LTV) 5 year closed LR 3.59% (75% LTV) 5 year variable LR 3.10% Stated Income Mortgages are still available for Self Employed Clients, not including commissioned or sales individuals.

Denise Pisani

(Lic #M11002770) Mortgage Broker at The Mortgage Centre Franchise Get A Better Mortgage Lic#10874 Office: 905-566-5363 Cell: 416-629-5363 www.MortgageInTheCity.ca

Refresher of the 3 New Mortgage Rules that have been in affect since January 2018: (courtesy Denise Pisani, Mortgage Broker)

1st Rule: Stress Test Starting on January 1, 2018, the Office of the Superintendent of Financial Institutions (OSFI) has set a new minimum qualifying rate, or “stress test” for all prospective home buyers, even those with a down payment of over 20%. Before the new, tougher rule, only buyers that had a down payment of less than 20% had to make sure they could pass a stress test. Regardless of how much money you save for a down payment, if you don’t pass the new stress test, the bank won’t give you a mortgage. Under the new mortgage stress test, potential home buyers need to qualify for a mortgage at a rate that is the greater of two indicators: either 200 basis points (2%) higher than the mortgage rate they qualified for, or the Bank of Canada’s five-year benchmark rate. Before the new stress test, home buyers or owners qualified at the rate offered by the lender. The actual mortgage payment will still be paid at the negotiated rate, but a higher calculation is used for qualifying purposes. 2nd RULE: Enhanced Loan-To-Value Measurements Traditional mortgage lenders (Canada’s big banks) need to ensure the Loan-To-Value (LTV) ratio remains “dynamic.” That means, it needs to be adjusted to local market conditions. The OSFI insists that lenders (excluding private lenders) have internal risk management protocols in higher priced markets, like Toronto and Vancouver. A LTV ratio is a number that describes the size of a loan compared to the value of the property. Canada’s big banks use the LTV ratio to determine how risky a loan is; the higher the LTV ratio the greater the risk. For example, if property values decrease following a housing bubble, the LTV ratio could actually rise and be higher than the total value of the property. In which case, it’s quite possible that you have negative equity in the house. 3rd RULE: Restrictions Placed on Certain Arrangements to Avoid LTV Limits Mortgage lenders (again, this does not include private lenders) are not allowed to arrange a mortgage or other financial product with another lender that gets around the maximum LTV ratio or other limits placed on residential mortgages. If you apply for a mortgage with a LTV ratio of 80% and the lender can only approve you for 60%, in the past, the lender could partner with a second lender for the additional 20%, bundle it together to get a complete LTV loan of 80%. Meaning: previously as brokers we were able to do a 1st mortgage at a BANK and do a PRIVATE 2nd mortgage with clients putting as low as 10% down! This can NOT be done anymore! Traditional lenders cannot do this anymore. |

* from Bank of Canada